The first step in creating jobs and continuing economic growth is to get a clear picture of our recent economic history, so that we will not repeat the mistakes that lead to the financial crisis. The financial crisis of 2008 cost our economy 8 million jobs and cost American families more than $16 trillion dollars of net worth. Bill Foster served on the Financial Services Committee during the emergency intervention that was required to avoid another Great Depression, and understands that it will take time to repair the damage caused by a decade of economic mismanagement. This means restoring fiscal discipline to our government, re-balancing our economy, improving the health of U.S. manufacturing, rebuilding the middle class and reforming Wall Street to prevent a crisis like this from ever happening again.

The 2008 Economic Collapse and the Emergency Intervention

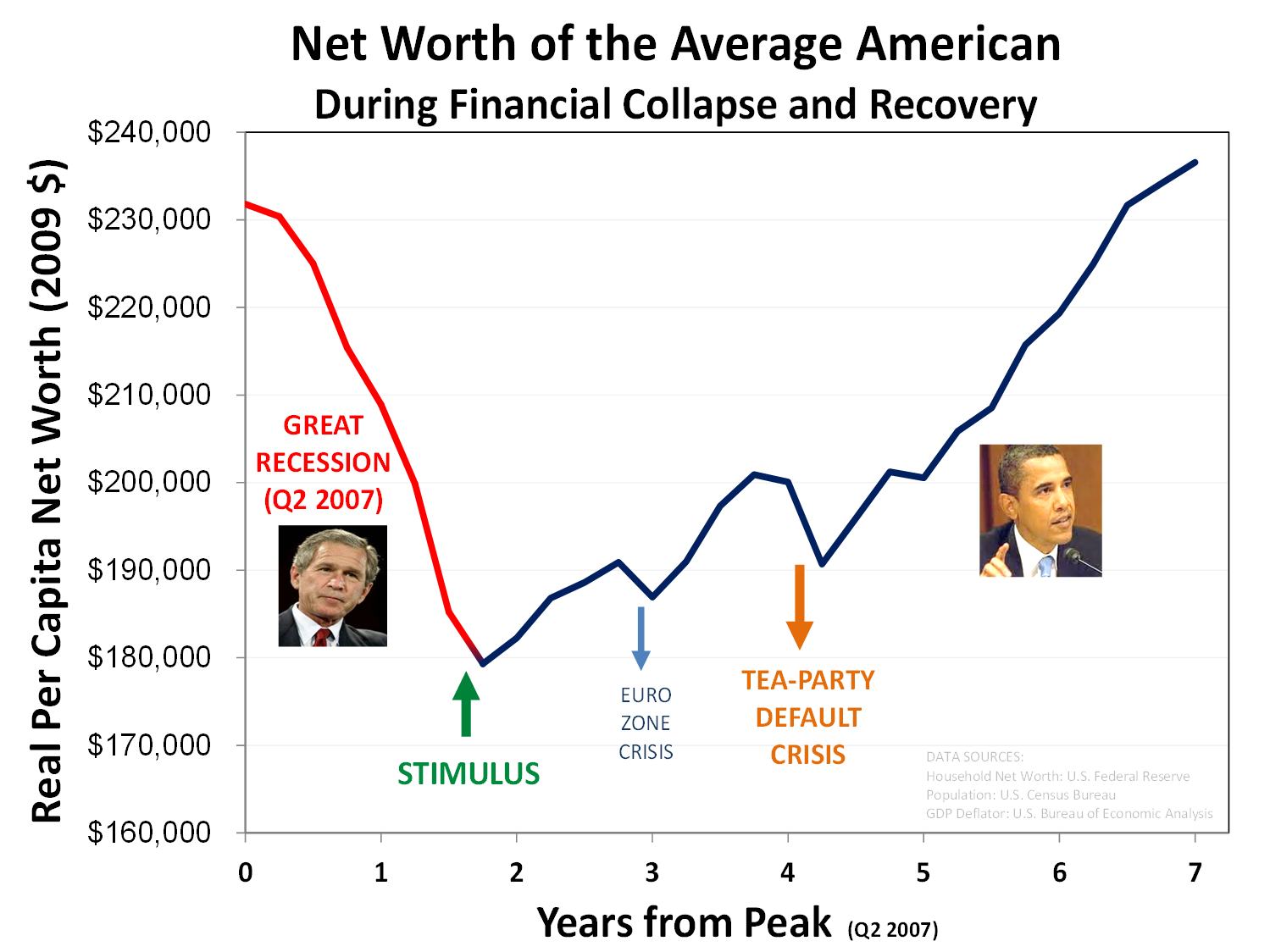

Families in the United States faced their worst economic conditions in generations as a result of the 2008 crisis. In a period of 18 months, household net worth – the total of everything a family owns: its house, retirement funds, bank accounts, and any small businesses it owns – dropped by more than $16 trillion dollars. This is more than $50,000 for every man, woman, and child in the United States.

As a businessman, Bill Foster supported three crucial steps for economic recovery:

1) An emergency intervention to prevent our economy from spiraling into another Great Depression. This intervention included cutting taxes to their lowest point in 60 years and making targeted investments in our economy. As a result, a depression has been avoided, retirement funds are recovering, business profits and household net worth have surpassed pre-crisis levels, and jobs are being created at the highest rate since the Clinton years. Unfortunately nearly ten years of bad economic leadership and misplaced priorities created this recession, and it will take us years to get out of it.

2) Restoring balance to our economy by reversing the economic mismanagement of the last decade. This includes returning to fiscally responsible practices with government finances, reforming broken trade policies, improving the business climate, and reviving the health of U.S. manufacturing. As a businessman who started a company that now provides hundreds of good manufacturing jobs here in the Midwest, Bill Foster knows what it takes for businesses to grow.

3) Reforming Wall Street to make sure we never again face a preventable crisis like economic disaster of 2008. As a member of the Financial Services Committee, Bill played a strong role in crafting legislation that will prevent the irresponsible practices that led to this crisis while ensuring a stable and efficient Financial Services industry for decades to come.

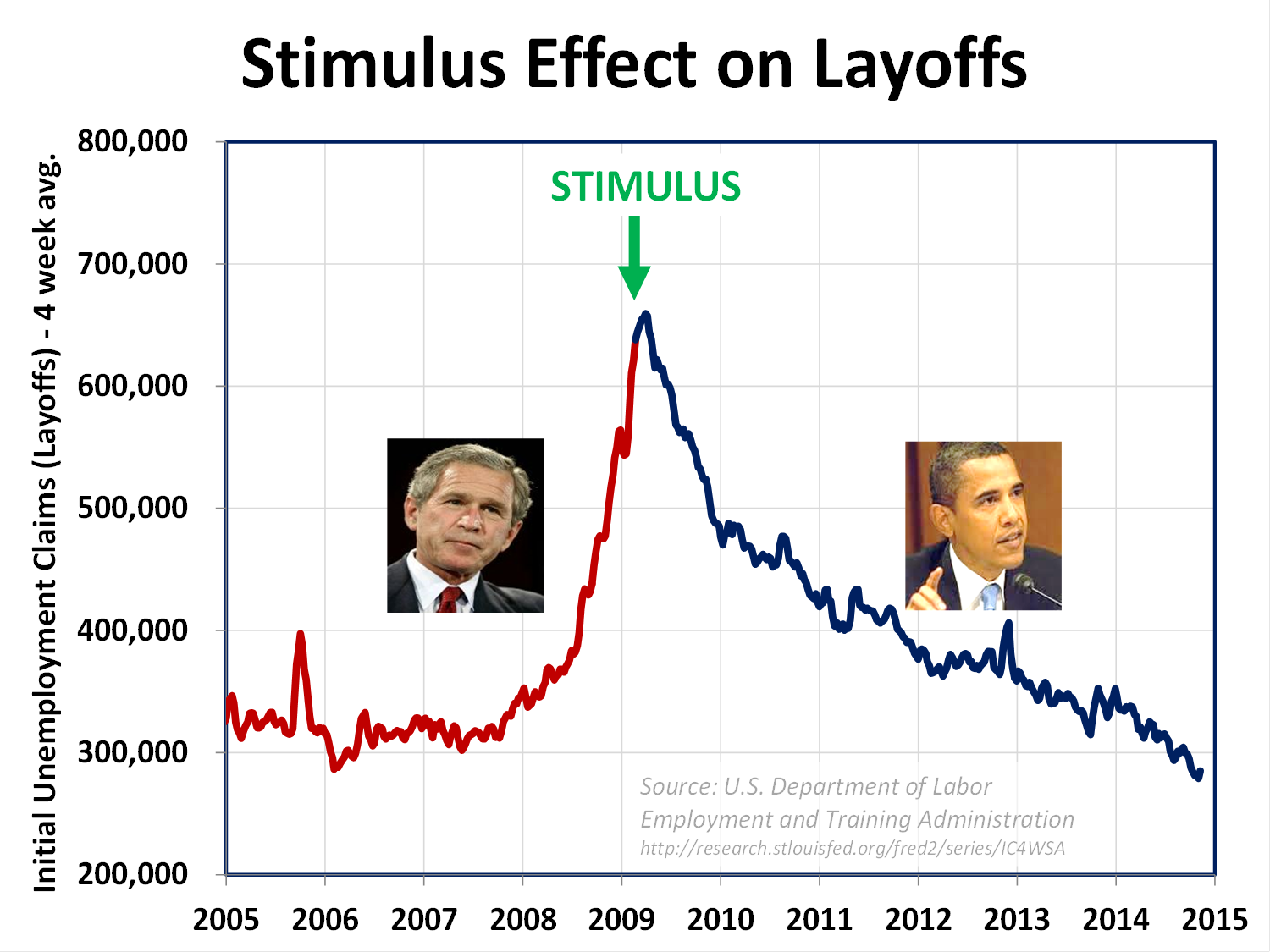

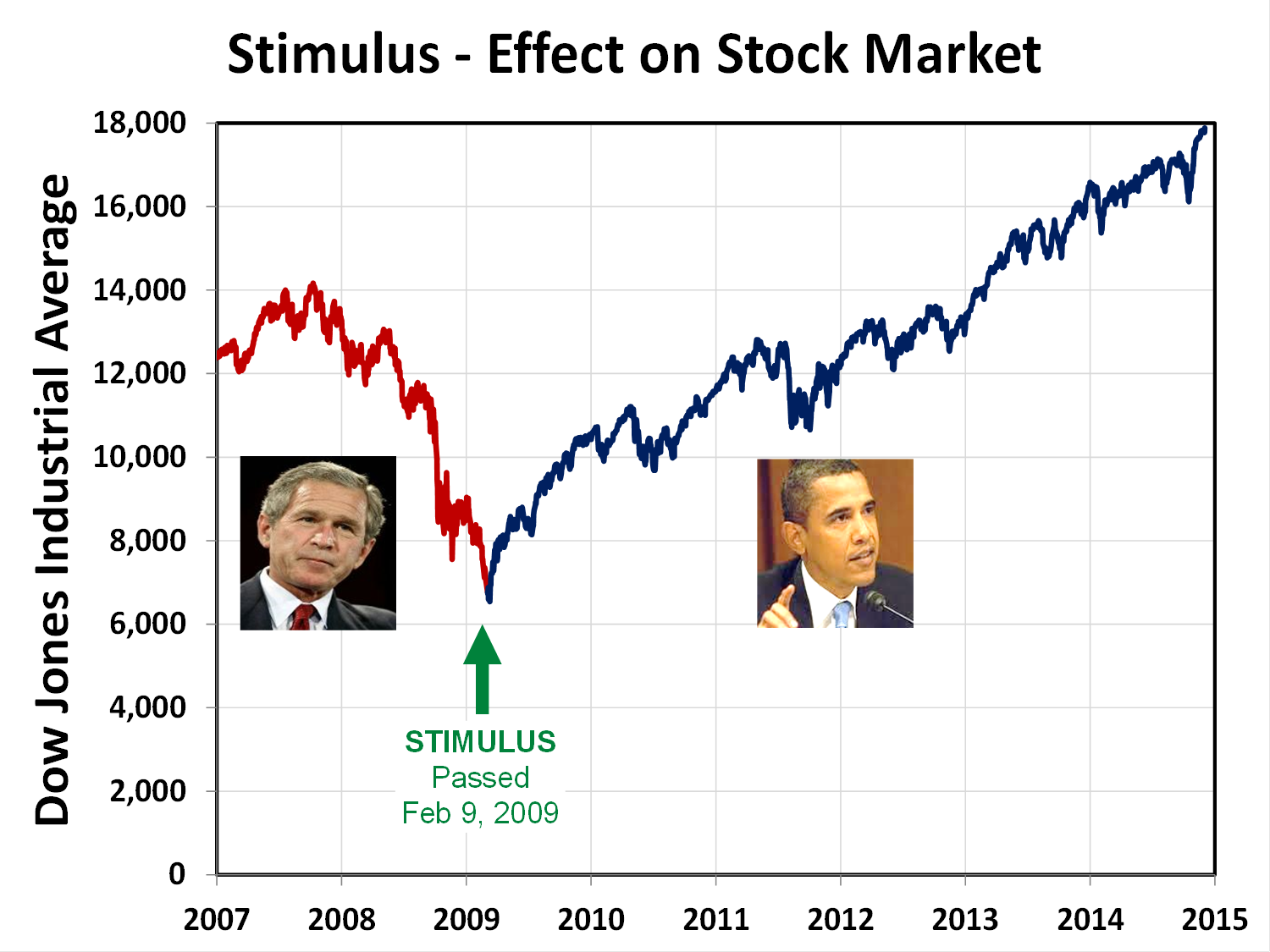

The Emergency Intervention: In response, Democrats put in place a targeted intervention to stimulate our economy: Tax cuts for small businesses and individuals, making funds available to banks, unfreezing lines of credit, providing incentives for consumers to buy homes, a fiscal stimulus to temporarily replace the drop in private-sector demand and to begin rebuilding our infrastructure, and extending benefits for the unemployed. Republicans uniformly opposed these policies, predicting runaway inflation and economic collapse.

The Economic Recovery: These Democratic policies triggered a V-shaped recovery which has now exceeded pre-crisis levels. Household net worth has rebounded by more than $18 trillion dollars, job creation is back at levels not seen since the Clinton years, and the deficit has dropped by two-thirds. Under Trump, the rate of job creation has not increased but the deficit has soared due to Trump’s tax cuts for the wealthy.

The recovery has been interrupted only twice: by the Eurozone crisis of 2010 which was caused by the failure of Europeans to restore Dodd-Frank style soundness to their banking systems, and by the Tea Party Default Crisis of 2011 (the ratings downgrade caused by newly-elected Republicans threatening to default on U.S. debt) which cost the Stock market over $1 trillion dollars and cost the average American over $10,000.

The Remaining Work: Although, on average, household net worth now exceeds pre-crisis levels, our economic recovery has not been widely shared. Over 90% of the benefits of our economic recovery have gone to the wealthiest few percent. This has been aggravated by the regressive nature of Trump’s tax cuts. Republicans continue to block Democratic efforts to ensure the recovery is widely shared by raising the minimum wage, reforming our tax code so that billionaires no longer pay taxes at a lower rate than hard-working Americans, investing in education and restoring the bargaining power of workers.

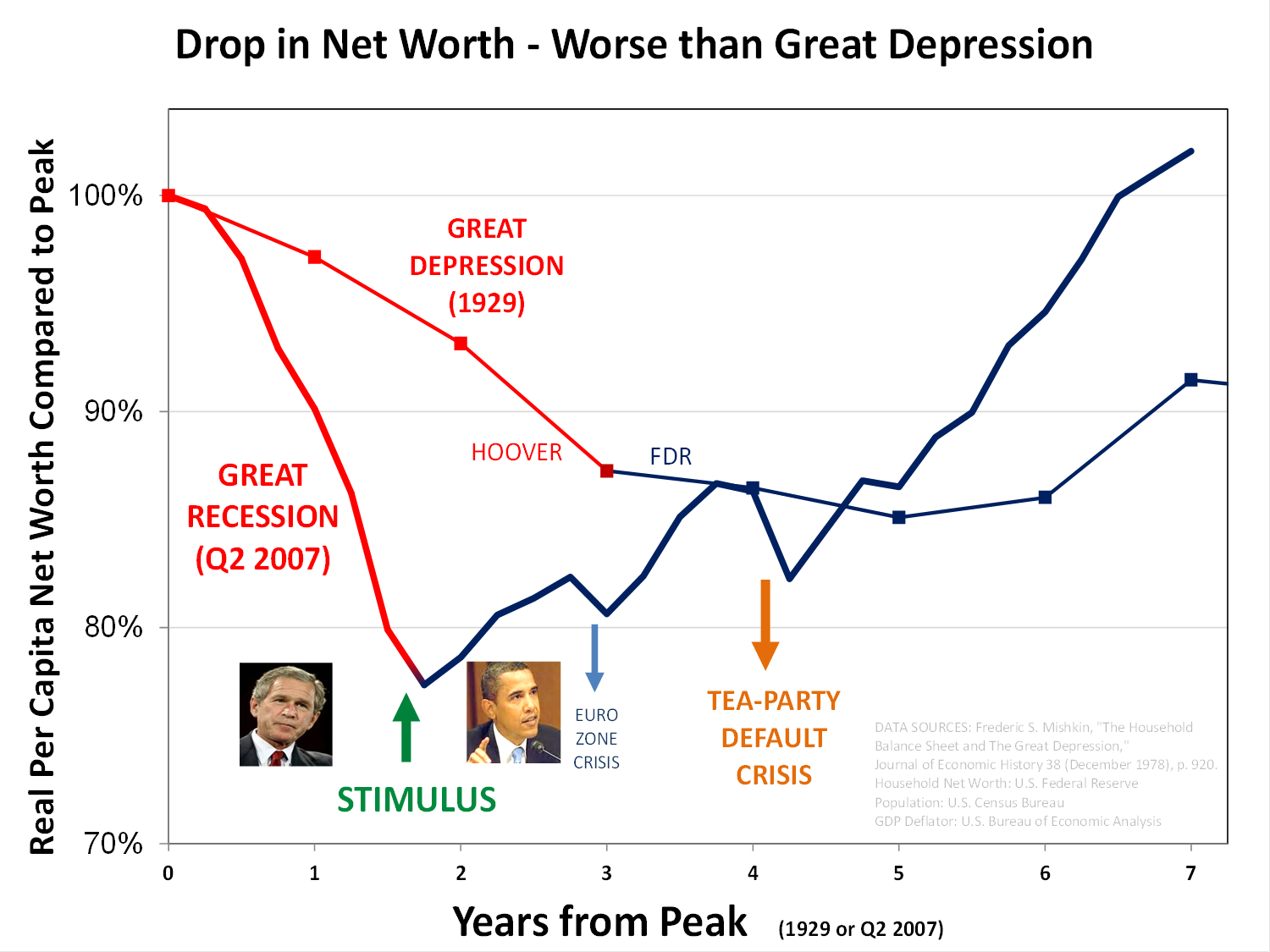

WORSE THAN THE GREAT DEPRESSION

The hit that our economy took during the financial crisis was actually worse than in the Great Depression, and the recovery was been much faster. At the start of the Great Depression, real per-capita household net worth dropped by 12% over a period of three years from 1929-1932. In contrast, household net worth dropped by more than 23% in a period of 18 months ending in March 2009.

In retrospect, it is remarkable that our economy did not fall into a full-blown recession following the 2007 collapse. Although the downturn was two times worse than the Great Depression, the recovery has actually been more rapid.